MyWebInsurance.com is your expert navigator to health insurance USA plans for 2026. Unlike direct insurers or marketplaces, it offers easy-to-understand actuarial summaries of ACA marketplace levels, employer plans, and Medicare, with easy comparison charts of costs and leading insurers such as UnitedHealthcare or Kaiser Permanente.

Table of Contents

Why MyWebInsurance.com?

This comprehensive insurance portal puts HMO/PPO and out-of-pocket costs and subsidy eligibility into one easy-to-navigate guide, bringing you individualized ideas by family size, health, and budget.

No blaring discounts, just straightforward, expert health, life, auto, and other insurance coverage updates for 2026, including premium increases and the new ACA.

Begin at MyWebInsurance.com now: you plug in your info and receive your own custom health plan comparisons at all the major insurance carriers, help you bypass the pitfalls, AND insure yourself without excessive, overwhelming coverage. Safety first!

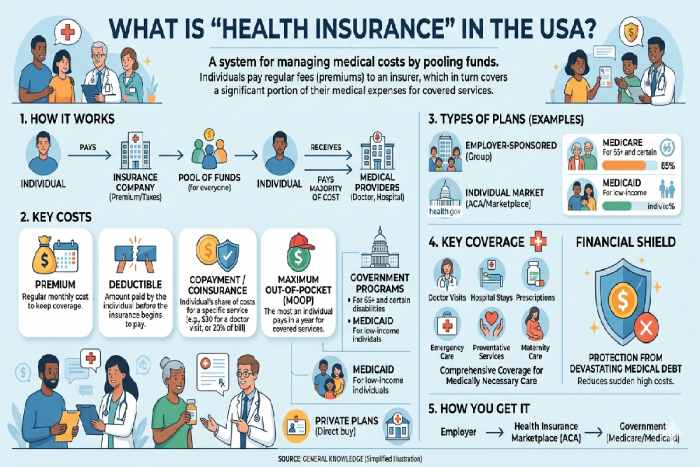

What is ‘Health Insurance’ in the USA?

Health insurance in the USA is an agreement between the insurer and the individual where the insurer agrees to pay part of the individual’s medical expenses in return for the payment of the premium. Your coverage will be determined by extending or not extending the coverage for doctor visits, hospital visits, emergency treatment, preventive care, and drugs.

Key points to understand:

- ACA regulations for most health plans operating in the United States regulate pre-existing condition coverage limitations and ensure the offer of essential health benefits.

- The ACA also created the federally operated HealthCare.gov and some state-based insurance exchanges, where families and individuals could shop for plans and determine subsidy eligibility.

- You may be surprised by just how expensive it is to suffer a major accident or illness without insurance

Main Types of Health Insurance in the USA

The US health insurance system is a mix of public and private options.

ACA Marketplace Plans

These are plans available for purchase from the federal HealthCare.gov or from state marketplaces, in four tiers available: bronze, silver, gold, and platinum.

- Bronze: the lowest premiums, the highest out-of-pocket expenses.

- Silver: a middle tier, often with cost-sharing reductions for eligible low-income enrollees.

- Gold / Platinum: will cost more in premiums but will have less in out-of-pocket costs.

Employer‑Sponsored Insurance

A significant proportion of individuals obtain insurance through their employment. Employer-sponsored plans tend to be the cheapest method of coverage.

Medicare and Medicaid

- Medicare is available to most people aged 65 and over and some disabled people under 65.

- Medicaid and CHIP cover low income individuals and families, with program eligibility and structure varying from state to state.

Short‑Term and Catastrophic Plans

Short‑term plans are not ACA‑compliant and can deny coverage for pre‑existing conditions. They are meant for brief gaps in coverage, not long‑term protection.

Private / Broker‑Sold Plans

These plans, often sold through brokers or online quote platforms, can be ACA‑compliant or non‑ACA depending on the product. Sites like mywebinsurance.com help users compare options from multiple carriers in one place.

How Health Insurance Pricing Works

In the U.S. Insurance primarily centers around 5 or so numbers related to the insurance coverage.

- Premium: This is how much money you will pay on a monthly basis for the insurance.

- Deductible: This is how much money you will have to spend out of pocket for healthcare services before the insurance will pay.

- Copay/Coinsurance: This is the dollar amount you will be responsible for the service; it is usually a flat amount or you will pay a percentage of the service’s cost.

- The out-of-pocket maximum: the amount you will be responsible for during the year, at this amount 100% of services are covered by insurance.

Insurance premiums are set according to factors such as age, region, policy, and family size; however, it is illegal for an insurance company to raise the rates due to a pre-existing condition.

Average Health Insurance Costs USA (2025-2026)

According to current nationwide estimates, an average premium for individual insurance can range from around $400- $600 monthly. This cost varies by age, region, and level of plan. Family coverage can range upwards of $1000- $1600+ each month prior to subsidies.

Key patterns:

- California, New York, and New Jersey are examples of states that tend to have higher-than-average premiums.

- States that are less expensive to live in, and have fewer regulations may have lower premiums for similar coverage.

- In the ACA marketplace, subsidies can decrease monthly premiums to less than $100 for eligible families.

Which Plan Is Right for You?

Selecting a health plan is about more than just finding the cheapest monthly premium; it involves careful consideration:

- Determine your needs: They are dictated by such factors as age, family size, household income, medical status and choice of physician.

- Note required benefits: You will likely be visiting specialists frequently, need ongoing maintenance medications or require only emergency coverage.

- Go beyond the numbers: investigate the premium, deductible, out-of-pocket max, and the network.

- Evaluate subsidies: subsidized premium estimates can be found using the marketplace or with a broker.

- Educate yourself about the plan: Be sure to review the list of covered drugs, the hospitals, facilities, and providers included within the network, and any applicable co-payments before enrollment.

If you‘re unsure, a helpful comparison engine that shows you many carriers at once makes this a lot easier.

What are the top 5 health insurance plans in the USA?

According to the market share, the top 5 health insurance plans in the USA for 2026, by number of enrolled, total gross premiums written are: UnitedHealth Group, Elevance Health, Kaiser Permanente, Centene Corporation, Humana.

Ranking approach

Over 40% of market share remain shared by these providers across AM Best & NAIC reports from 2023 to 2025. The market share is based on a combination of net premiums (over $200B total), number of enrollees, and customer satisfaction data from J.D. Power, as well as the size of the network (millions of providers).

Comparison Table

| Rank | Company | Market Share | Members (Millions) | Key Strength | |

| 1 | UnitedHealth Group (UnitedHealthcare) | 16% | 49+ | Biggest network, employer plans | |

| 2 | Elevance Health (Anthem) | 12% | 47 | Affordable ACA marketplace | |

| 3 | Kaiser Permanente | 7% | 12.5 | Integrated care (HMO model) | |

| 4 | Centene (Ambetter) | 11% | 28 | Medicaid focus, low-income | |

| 5 | Humana | 5% | 17 | Medicare Advantage specialist |

UnitedHealth leads broadly; Kaiser excels in quality for West Coast users.

How MyWebInsurance.com Stacks Up Against Other Life Insurance

When you compare MyWebInsurance.com to other popular U.S. life insurance tools like Policygenius, Haven Life, Bestow, and Ladder, you’ll see clear differences in how each platform works, what they offer, and how you ultimately buy a policy.

| Feature | MyWebInsurance.com | Policygenius | Haven Life | Bestow | Ladder |

| Online comparison | Compare multiple carriers in one place | A marketplace that shows many carriers | Not a marketplace (direct insurer) | Direct insurer | Direct insurer |

| Direct policy issuance | No — connects to carriers | No — broker | Yes — policies issued (MassMutual) | Yes — online term life | Yes — digital term life |

| Agent support | Limited (mostly DIY tools) | Yes — licensed agents help guide you | Licensed reps for existing policies | Yes (online support) | Yes (digital support but limited agent guidance) |

| Life insurance policy types available | Term, Whole, Universal options for comparison | Term & Whole (plus other financial products) | Term life only | Term life only | Term life only |

| User interface | Easy research and comparison interface | Medium — robust info and agent tools | Easy, fast, digital‑first | Medium, simple application | Easy, modern online experience |

Conclusion

Picking health insurance in the USA doesn‘t have to remain complicated; get the basics, know what you need, study how premium & out-of-pocket costs compare at the best companies (UnitedHealthcare, Elevance, Kaiser, Centene, Humana), and use the simple mywebinsurance.com for side-by-side quotes from several dozen insurers. Tools like mywebinsurance.com compile options, project subsidies, and then tell you how to enroll more easily than a marketplace. Start your search for health insurance in the USA today to find coverage for your 2026 budget that keeps your family safe.